No overview table yet. I still haven’t gotten around to take the measurements. I keep my focus on my exercises and adding something to them every week. As explained last month, slow and steady progress is the name of the game.

So how did I do on the this front?

Let us see for the 3 catgories of exercises I do now.

Fitness

Once more I didn’t miss a single fitness day and continue to add some weight and some exercise repetitions. Even with this slow and steady approach the gains are significant over a one month period!

At the time of my last health report I lifted 14 375 kg. And in the week of 16/05 I lifted 15 504 kg! That is an extra 1 130 kg added! Remember, I started out around 5 000 kg.

I repeat once more that progress in weight lifted will be slower going forward as I am going to stick to my ‘adding a little bit every week approach’. I also have added kettlebell swings to my greasing the groove routine. This is an extra weight exercise but I am not tracking it in the fitness app so it doesn’t show up in the above overview.

Greasing the groove

This keeps being the part of my regime I enjoy the most. Believe me, I find it crazy too that I like this so much! But it seems to be working very well for me.

I have reached my interim goal of 25 reps so for the last two weeks I did 8 times x 25 reps x 6 days a week = 1 200 + the 50 sit ups I do on Sunday which brings me to 1 250 crunches in a week. As you can see having vague goals and not worrying when you reach them eventually does lead to some impressive results!

Honestely, I do not even care when I will reach my final goal of 50 reps. The goal is to keep doing this every day, every week and every month and eventually I will reach that goal.

Actually, progress on the crunches will also be slower since I now have added the kettlebell swing exercise to my routine as off this week. I did 8 reps x 6 days with a 4 kg weight. The 4 kg weight is definitely to low for me but it is what I have for the moment. I will first build these reps up to 25 also and once I reach that I will double the weight, drop the number of reps and then slowly build up the nr of reps once more.

And yes, I did do my sit ups at the office the one day I went. I just popped into an empty meeting room and got crunching. Add the kettlebell swings and I am going to be getting some strange looks once the working from home restrictions are lifted!

Cardio

A bit of some good and bad news on the cardio front.

On het bad front: I missed 1 rowing session! And I missed it on the one day I went to work at the office!! This has gotten me a bit worried that since I build up this exercise routine while working from home I will not be able to stick to it once I go back to the office. Our new work agreement does allow us to work from home 3 days a week. But I hope to be able to push this to 4 days (the days I do my fitness). I then just have to make sure I do my rowing on the day I do have to go to the office.

The good new is I did keep adding 1 minute to my rowing time every week. This week I reached 16 minutes. It is starting to get tough to keep it up. So I’ll probably hit a plateau in the coming month, but that is fine. 16 minutes of rowing is already pretty good. Every minute I can add to it is a win!

Belgium was still pretty much locked down so April was another month of low spending for me. In the first 4 months of 2021 I have spend a total of 5 910,50 euro which means that on average I have stayed within my 1 500 euro monthly budget. And that includes the purchase of a 800 euro rowing machine! I think it is the first time ever that I was still within budget 4 months into the year!

Let’s take a look at the numbers of this month.

Income: 2 277,55 euro

Expenses: 1 428,50 euro

Savings: 849,05 euro or 37,28%

Income:

Income was my pay slip from work plus a 100 euro gift from the parents because of easter.

Expenses:

Expenses are going slightly higher but this was in part by design. With the country slowly opening up I used this month to buy some more essentials as I am hoping to finally be able to spend some money on going out and seeing people in May.

First are the fixed expenses I need to pay each month.

This includes the 1 100 euro I transferred to our joint account for my part of the mortgage,utilities, groceries and such ,,,

My mobile phone subscription of 12 euro (no reduction this month).

A medical bill of 10 euro. Back in February I hurt my richt ankle (again) and just to be on the safe side I had photo’s taken form than foot (it was just sprained). The bill for this came in April.

Then there are a few moments of weakness.

Steam once more seduced me into buyning another game, No man’s sky set me back 54 euro.

I also spend 50 euro on extra food. Most of it was in line with my regime, but not all of it.

And then there was the stuff I decided to buy in April since I was going to end the month below budget anyway.

95 euro went to a new keyboard and mouse as working from home has taken a toll on my home equipment. Fancy new led lights, mmmhh! I actually only needed a mouse and I could have gotten one from work for a few months but I want decent stuff to work with and even pre-Covid I was thinking about buying me better gear for the work place. Now that I work from home there is nothing stopping me setting up my workplace the way I want.

I could have used the Vespa a little bit less and pushed the refill to May but we had a few very nice weather days in April and I enjoy riding my Vespa more than I do using the car so I filled it up in April: 10 euro

With all the exercise I am doing I needed some extra sport outfits. I have been rocking the same short for the last year and it was porbably 10 years old to begin with. I also needed some new underwear. And I define ‘needing new cloth’ not because ‘the colors are a bit faded’ of ‘it went out of style’ but more by the number of holes and how big they are. Trust me when I say I needed them.

All of this on the below photo set me back 97,50 euro.

I may have gone a bit over with the shorts. If my current use of 1 short per decade is any indication this may very well be the last shorts I will buy during my lifetime.

I am going to try to do these health reports on a monthly basis again. The old overview table will come back and will be updated again.

But I haven’t gotten around to retake the measurments so this will be for next month. I try to be less focussed on my weight and measurements and just add something extra to an exercise each week. This makes for slow progress but it should be a steady progress. In the past I had these very strict goals to achieve X by date Y. Which resulted in me either getting demotivated because I did not achieve the goal and stopping altogether. Or me getting injured, needing to rest for a couple of weeks, and that rest usually ended in me quitting completely…

Slow and steay progress is the name of the game now and every progress I now consider a WIN. It’s a lot more motivating than my old approach and for now it seems to keep me continuing.

Fitness

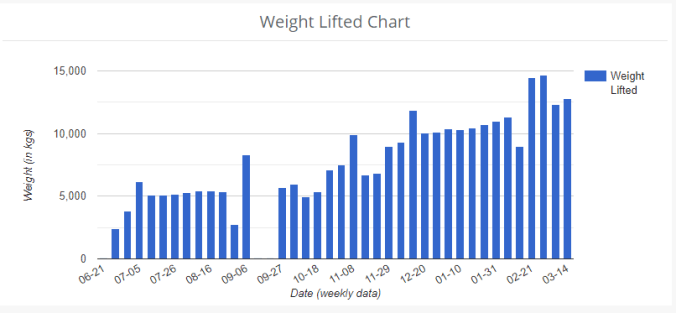

I didn’t miss a single fitness day since my last health report. And I have added a bit of weight to several exercises. The weight lifted chart tracks this increasy nicely.

I have no explication for the exceptionally high bars now and then. Best guess is that it are tracking anormalities, even though I try to log the exercises as correctely as possible.

This graph does show the benefits of the slow and steady approach. Where in the week of 16/08/2020 I only lifted a total of 5 436 kg. At the time of my previous update, the week of 28/03/2021 I had lifted 13 176 kg. And this week saw me lifting a total of 14 375 kg! It is already a certainty that by July 2021 I will have more than trippled the lifted weight (5000 kg I started with). Slow and steady progress over a longer period leads to impressive gains. Progress in weight lifted will be slower going forward as I am going to keep my approach of only adding 1 kg to an exercise every week. And adding 1 kg when you are pushing 10 kg is a 10% increase where adding 1 kg when you are pushing 20 kg is only a 5% increase. But the approach is working and it should keep me injury free while I continu pumping iron.

Greasing the groove

This might be the part of my regime I enjoy the most. It is only 1 minute of exercise 8 times a day but it does lead to impressive numbers.

At the end of March My regime was 8 times x 16 reps x 6 days a week = 768 crunches and with the Sunday included actualy 800 crunches that week.

Even after plateau-ing at 20 reps for 2 weeks I reached 21 reps this week. So that was 8 times x 21 reps x 6 days a week = 1 008 + the 44 I did on Sunday brings me to a total 1 052 crunches this week

Ultimate end goal remains 50 reps every hour but interim goal is 25 reps. When I reach this goal I will add kettlebell swings to my greasing the groove regime. Once those kettlebell swings are added I will alternate by adding sit-ups reps one week and kettlebell reps another week. Again, slow and steady progress and no time limit on when those goals need to be reached. Actually, I do not even NEED to reach those goals. As long as I add something every week I am doing good!

Cardio

Cardio is what should help me loose weight. Last month I explained why I choose rowing as my main cardio exercise.

I started at only 5 minuts of rowing my first week. But slow and steady also wins the race when it comes to rowing. Back in March I was already rowing 3 x 8 minutes a week and this week I reached 12 minutes! At the moment I am adding 1 minute to my rowing every week and I am sticking to it for the time being.

A focus on my health and another lockdown(which our government is calling a ‘easter break’) really helped keeping the spending in check.

Income: 2 177,55 euro

Expenses: 1 280,60 euro

Savings: 899,40 euro or 41,26%

Income:

No gift from the parents so just my normal income from work which stood at 2 177,55 euro

Expenses:

At 1 280,60 euro expenses were pretty low in March. They would have been ever lower ha dit not been for some obligated things.

First of is off course the 1 100 euro that went to our joint account for my part of the mortgage, utilities, groceries and such ..

But my health insurance was also due this month. It cost me a grand total of 74,40 euro.

I also received my annual cost for the use of my Visa card: 22 euro. I know I could get a free card via Keytrade or Argenta but for the moment we are stuck at the big bank due to our mortgage and I am too lazy to get another bank account just to avoid this cost. I have been looking into prepaid credit cards. But I can only find mastercards with no anual fee. Since my girlfriend has a mastercard I prefer to have a Visa card. Coverage isn’t exactely the same for both and it has been to our advantage in the past to have access to both networks.

Mobile phone was only 1,20 euro as we had accumulated enough points to get a reduction.

New sport shoes to use on the rowing machine cost me 50 euro.

I needed a new cable for my headphone which set me back 10 euro. Also in the entertainment section: a game on steam for 5 euro.

Townscaper lets you create very cosy little villages. It’s very relaxing!

Nothing for the Vespa as working from home has me almost not using it. I will need to fill up in April.

Rounding up the March expenses was 18 euro‘s spend on extra food. A better focus on my health kept the extra food expenses really low in March. Here’s hoping for a repeat in April!

Total expenses for the first three months now stand at 4 482 euro which means that on average I have stayed below my self imposed budget of 1 500 euro a month!

Average savings rate even hovers above 37%. Previous years this was more around 30%. this was off vourse for a full year so I will see if I can keep it above 30% for the rest of the year. My guess is savings will drop substantially once stuff starts opening up again.

The last health report I did was from October 2018. 2018 people!!

As is usual with these things, when the reports stop it usually means it didn’t go well.

My weight continues to be something I struggle with. I eat when I am stressed and work was plain and simple exhausting me. And the end of the day I was just mentally beat. So I started eating more. This remained reasonable as long as I kept swimming. But having the mental energy to go swimming was also running out …

I just didn’t have the willpower to swim for 2 km on end. In a last ditch effort I started to reduce how much I swam in the -futile -hopes of keeping the habit of going 3 times a week. I wanted to keep the habit in the hopes that the mental dip would be temporary and after a month or two I could bounce right back to the full 2km.

Well that didn’t help. Swimming dropped to zero. The weight kept stacking up and with the heigher weight the push ups became harder so those stopped as well.

Exercise was down to zero and I was eating all the time.

How bad did it get? 120 kg bad.

Somewhere around the end of 2019 I did restart swimming. Knowing I am going to do exercises usually helps to eat less as well (because swimming when you are all bloated isn’t very fun). It was slow going but I enjoyed it again and slowly training my way back to the full 2 km. Then the lockdown due to Covid happened. The week they closed everything was THE week I was going to do my first 2 km again.

Being pissed off was an understatement! By the time the swimming pool re-opened (under very ridiculuse Covid measure as well) I knew I would have to restart all over again. And I just couldn’t. Especially with all the uncertainty of a possible new closing.

I wanted something I had 100% full control over. Because if I was dependant on our government making smart decisions I could wait a long time.

Luckily I already had moved my exercise bench from my parents home to my home before the lockdown. And the plan had always been to start fitness once my swimming was a strong habit again. So I just decided to flipped the sequence and start with the fitness.

Over 30 years old this fitness bench still works lke a charm!

Fitness

I started with the fitness on 21st June of 2020. To keep me honest and being able to track my progress I decided to pay for an anual subscription fot the Jefit App.

I started low (because it had been a long time since I did this) and didn’t progress a whole lot until september. Did had two reasons, I had to get into the habit of regular exercise. Being 120 kg does not help with this. 120 kg is already a lot of weight to get moving .. I also lacked some weights to start adding in a gradual way. And since the start of this pandemic exercise equipment is hard to get because everybody started exercising from home. As a little side note, i would not invest in any stock from gym compagnies. With people having all the equipment they need at home I can see their membership numbers not really rebounding after Covid.

The gap in the picture below is our 10 day holiday in Portugal. And you do see chart starting to go up after that holiday because I finally received my weights ordered back in August.

I did make a stupid mistake between June and September: in the abscence of the necessary weights I could have increased my repetitions! It was only when I started modifying the weight in the app that I actually realised I could also modify the reps! STUPID (afbeelding).

So as of October I started adding something (either a bit of weight or some extra reps) to 1 or 2 exercises.

It might not be all that much fitness I do, but I do I have now been doing it consistently since the 21st June, which brings me to 9 months at the moment!

Add it all up and total numbers start to be impressive:

Could I have pushed myself more in the fitness department? Probably. But I like my current approach and seem to be able to keep doing it. And that in itself is a big win for me.

The only thing I didn’t like with my exercise regime was that I didn’t make a lot of progress with my sit-ups. The orignal plan only had once a week 3 x 8 crunches. This was a bit low to make any decent progress. So I added crunches to another day as well. This helped but progress was still low. I used to do A LOT OF crunches when I was young and miss those days. Enter greasing the groove.

Greasing the groove

A co-worker mentioned greasing the groove as a way to make some serious progress in a specific exercise. It basically comes down to doing a lot of reps but spread out over the day and only at around 50% of your maximum. I like this approach, I have never been fan of the ‘No pain, no gain’ school of fitness. In general I like to avoid pain (self inflicted or not) as much as possible in my life.

Since I had slowly worked my way up to 3 x 20 reps of crunches twice a week I decided to start with 10 crunches 8 times a day, for 6 days a week. Sunday is rest day, except for a one time crunch session to determine my new max.

So I went from 3 times x 20 reps x 2 days a week = 120 crunches per week.

To 8 times x 10 reps x 6 days a week = 480 crunches per week.

Add in the Sunday where I determine my maximum reps I can do I did 500 sit ups in my first week of greasing the groove.

This week my regime is 8 times x 16 reps x 6 days a week = 768 crunches, add in the Sunday and I have reached 800 crunches this week.

My current work environment with the exercise mat next to the desk so I can do my 16 runches every hour

My goal here? Well, remember how I used to do A LOT OF crunches when I was17 years old? A lot was 300 sit-ups, 5 days a week. I want to reach that goal once more! Actually, way back I did 3 x 100 crunches. I want to at least get back to 50 reps each and every hour. That would bring me to 2 400 crunches per week. This seems like a crazy amount of crunches but this is only trippling my current level and it would mean 2 minutes of exercise every hour. I can do 2 mins of exercise per hour!

Once I reach 1 500 crunches per week I will add a kettlebell exercise to my greasing the groove regime. And once my weight is back below 100 kg also push ups. Speaking of weight loss, enter cardio.

Cardio

Ok, so I have been doing fitness 4 times a week for the last 9 months.

The last three weeks I have started doing a lot of crunches.

How is my weight doing you might ask.

Holding steady at 120 kg …

So I went from a fat, out of shape sloth to a fat, kind of in shape sloth. But still fat. You know when I did lose some Kg’s? The 10 day holdiay in Protugal where we either biked or walked some distance every day (the girlfriend has this annoying habit of finding all these cool things to see on our holiday which usually involve walking). So yes, if I want to have any hope of actualy loosing weight I need to add in a cardio exercise.

I do not like walking (go ahead, ask me how much I enjoy our holidays …).

I do not like biking.

I do like swimming but Covid + our stupid politicians kinda sucked all the fun out of that one.

I also wanted something I could do in my house since our politicians seem to enjoy locking us up on random occasions.

Enter rowing! I remember liking it when I went to a gym back in my student years.

SO I bought a rowing machine. Financials details here.

Welcome to the modern age where people pay good money to torture themselfs!

It is slow going because cardio has been a while (March of 2020 actually) and rowing seems to use some muscles I haven’t used in a looong time. Next week will be my third week of rowing. I am at only 8 minutes for the moment. But the goal is to build this up to my level of swimming. 2 km of swimming took me about one hour. So I have a long way to go here.

Interim goal is reaching 15 minutes.

With so many things out off our control at the moment I do find it very soothing to know that all of this is in my complete control. All I need to do is go to our utility room and start exercising. Bad weather or a worldwide pandemic … nothing can interfere with me doing my exercises! Adding a rep, some weight, some extra crunches or extra time to my rowing, it can not be stopped!

Consider this my ‘one year of living with Covid’ post. If you had your fill of those you can skip this post as it will barely mention any financial stuff (which was also the reason why I didn’t mention anything Covid related in my 2020 full year recap post.

Although Covid was already present before, the first real impact in my life was when the spread of Covid-19 forced Belgum in it’s first lockdown. This made working from home obligatory for everybody that could. From one day to another, the roads in Belgium were empty.

Working from home

This went pretty well for me. At my work this had always been a possibility but was usually only used for the occasional day when a big delivery was expected or a contractor was performing some renovations at your home. So the possibility already existed. This made planning for a full shift where everybody was working from home all the time easier.

My girlfriend works in the healthcare sector so there was no working from home for here. The only real problem we had was that our office room was not yet fully renovated. Which meant my desk was in the living room. This was a bit annoying for the girlfriend since she sometimes had a weekday off. So I did occasonally go for one day to the office. It was a bit strange being with only 2 or 3 people in an office meant for 60+ people. But that did make it VERY safe to go to work for me off course.

My office with a cheap 5 euro desk since my real desk is a ’70s monstrosity that weighs a ton and I am planning on moving that behemoth only ONCE

Once our office room was finished (only thing left to do now is placing the skirting boards) I moved into the office room and since then working from home has been smooth sailing. I do not miss the daily commute to work and since June I got in the habit off doing my fitness exercise during my lunch break (more on this in my upcoming health report). I do realise we are lucky in this regard as we have a large house with a seperate office room and enough space to put some fitness equipment. The large garden also helped (no full parks for this guy!)

The small orchard part of our garden during spring last year

Health during Covid-19

We did have a big scare when the girlfriend was infected with Covid in March (the perks of working in the health sector!) mainly because it was early days of the pandemic and there were many unknown about the disease then. It’s also a scary disease because it attacks the lungs and difficulty of breathing is very scary. No hospitalisations was required. No hospitalisation is a good thing but with the difficulty of breathing and the fact we sleep in seperate bedrooms did have me worry A LOT during the worst days of her infection. I worked from home and I did have two mornings were I quietly snuck into her bedroom to go check if she actually was still alive or not. In all honesty I am a bit mad at our government for dialing up the FEAR dial a bit too much here.

I myself never caught Covid, despite being in the same house as the girlfriend for the whole two weeks and we aren’t clean freaks either. And in the meantime the girlfriend has made a full recovery and health wise we are both fine at the moment.

Financial impact

Since we both kept our job and kept on working during the pandemic (well except the two weeks the girlfriend was sick) there was no impact on our income. Covid did have us spend less I think. For me it probably is a wash as I am a pretty frugal guy under normal circumstances and I did buy some home party equipment. But the girlfirend, who does enjoy going out, reports she did save more the last year.

Laser, smoke machine, I love the internet and it’s ‘no matter how crazy you can buy it here’ powers

Mental health

Mental health wise we both are pretty fed up with the whole situation. Living 100+ km form friends and family has made us some of the most isolated people in Belgium during the last year. We had a garden party with 11 friends in July, a very small party in our living room in August with 4 people and we went to see some friends in Ghent in December. And that is the full sum of us being social for the last year. I had about 20 work days where I saw some co-workers (and work is busy, so not a lot of time for socializing), the parents a couple of times and a few neigbours- at a distance.

I am not a people person, but this shit is starting to be ridiculous. I also did a pretty good job at ignoring the news, before Covid. The pandemic kind off sucked me right back in. And honestely, there was a reason I was ignoring the news. Our news sucks, our government sucks (at several domains, the handling of this pandemic being the biggest one off course) and I long for the days I can all ignore it completely once more …

We can now again meet up with 10 people in our garden. I am now eagerly awaiting the return of some better weather (a hail storm just past over our house yesterday afternoon) and then I am planning on having back to back garden BBQ’s and outside parties.

Last year I had almost no change to use my fancy new Rocketstove

Februari was a cheap and expensive month all rolled into one. Cheap because I hardly bought anything at all. Expensive because I did spend a lot of money. How is the possible? Full explication is below, but first the numbers:

Income: 2 677,55 euro

Expenses: 1 962,20 euro

Savings: 715,35 euro or 26,72%

Income:

With almost 2 000 euro in expenses my savings rate for March was saved by the income side.

2 177,55 euro of income was from work and an extra 500 euro was a gift from the parents. When they heard I was planning on buying an extra piece of exercise equipment they offered to pay a big chunk of it. Read the expenses to find out what exactely I bought.

Expenses:

Once again I transferred 1 100 euro to our joint account (mortgage, utilities, joint grocery shopping …)

Extra food was 46 euro. Helped by a short month and working from home I didn’t eat that much extra! Actualy lost a little bit of weight and no that was not due to the exercise equipment I bought!

Mobile phone was 5 euro this month.

Gasoline for the Vespa was 8,20 euro. Working from home means I hardly use the Vespa. I could not use it all but leaving it stationary for months on end wouldn’t be very good. And I enjoy riding it, even if it still cold out. So I use it short trips to somes shops (extra advantage: no parking issues). Which does mean that on occasion I do need to fill up the gas tank. Februari was one of those occasions. I am curious if I will make it to April before needing another refill.

Exercise equipment: 799 euro. With the extra weights purchased last month and also Octobre last month I am set for my home gym except one important aspect: cardio.

I already had a full exercise weight bench from my youth. So I only needed some extra weights.

The exercise bench that kept me in shape when I was young

But for cardio I had nothing and with weights only I am not really losing weight. Yes, I do know you can lose fat with weights only but your power training regime needs to be a lot heavier than what I am doing. I have zero ambitions to go this route. So some kind of cardio was necessary.

I will delve into the exact reasons why I chose rowing in my health report (which I pinky swear I will publish in March, well perhaps April…). But for 799 euro I bought the Cobra XRT plus 2 from Hammer.

No worries, it folds so is not blocking our washing machine andryer aal the time!

The Cobra XRT plus 2 is a midrage row trainer that should give me years of exercise torture! With an annual subcription for our local swimming pool at 250 euro 4 years of use should let me earn this money back! But if it improves my weight I am ok with it costing me money!

I didn’t use the rowing machine in Februari, because it arrived late on a Saturday, I spend 2 hours on Sunday assembling it in or pretty cold utility room and then on Sunday evening I hurt my ankle pretty badly! Which explains the 4 euro final expense of Februari to go visit my doctor! Nothing broken but those ligaments were pretty fubar! So it was only 3 March before I used the rowing machine for the first time. But I will delve into that torture in the upcoming health report …

The last day of Februari seems to me as the perfect day for a recap of the month Januari. Because .. if you know you’re lazay, clap your hands, … If you know you’re lazy clap you hands ..

Income : 2 222 euro

expenses: 1 239,20 euro

Savings : 982,80 euro 44,23%

Income:

Income was plain old boring work income plus a 50 euro end of year gift from the parents. The parents actualy gave me a bit more money at the end of year. But since most of it was destined for the purchase of a rowing machine. And since I bought that in February it made a bit more sence to als book the gift in Februari. All it does is moothing out the numbers a bit.

Expenses:

As every month, 1 100 euro went into our joint account to pay the mortgage, utilities and our joint grocery shopping.

Extra food was 61 euro. Once more, pizzahut is to blame!

I also spend 78 euro on extra weights for my fitness equipment. I still haven’t received the complete order as home fitness sales have apparently tripled over the last year and there is a huge backlog for everything. But once everything is delivered I should have enough weights for the rest of the year.

I don’t know about you guys, but I keep my weights on top off an old fridge ..

And that’s it. that’s all I bought in Januari. Lockdowns are cheap!

The bitcoins are worth 240 euro at the moment but I am planning on spending all my ill gotten gains in March. Darknet here I come!

It is starting to become somewhat of a habit to do these full year recaps on the first of February.

Which immediately anwsers the first question: yes I am still as lazy as I was back in 2019.

Since I liked the overview I did last year I will be continuing it this year. This is going to just be a financial recap of 2020. I am saving the whole covid stuff for a ‘1 year working from home recap’ which I will try to do on time . On time being 15 march 2021 as that was the start of the first lockdown in Belgium and since that date I have perhaps been to the office a grand total of 20 days.

4 year recap

2017

2018

2019

2019 corrected

2020

Income

30 862

27 765

39 221

34 221

32 064

Expenses

20 719

20 047

28 320

20 207

20 228

Savings

10 143

7 718

10 901

14 014

11 836

SR

32,9%

27,8%

27,8%

40,9%

36,9%

Recap conclusions

The trend from the last years seem to continue:

* my annual spending is slightly above 20 000 euro

* that spending is pretty much irrelevant from how much income I make

The sidegig did not materialize in 2020. Let’s hope I have some better lucki in 2021 on that front.

2020 numbers

Income

Income was 32 064 euro.

Working for the Boss man brought in 31 441,67 euro. The reason this is lower than 2019 is because I did not get a double bonus this year. My company has no ‘double bonus’ policy. It was very exceptional for me to get one last year. So this year is actualy a return to normal.

Gifts were 530 euro. With no new car to buy my parents didn’t see any reason to give me any extra gift except for the normal birthday, christmas and such gifts.

Covid did bring my little experiment with ticket arbitrage to a screeching halt.

I also got 89 euro back from my health insurer.

Expenses

Expenses totaled 20 228 euro.

Predictably most went to our joint account since we use that to pay our mortgage, utilities, food .. My half of all these bare necessities has cost me 13 400 euro in 2020.

Theoretically I could live on this amount. It wouldn’t be any fun at all, but I could, well exist on it.

The Vespa cost me 1 367,15 euro. Honestely I thought this was going to be a lot lower since I have barely used it since March when the pandemic hit and I started working form home. But I was close to needing some maintenance when the pandemic hit. So I didn’t really save that much on maintenance (890 euro) this year. I only saved on fuel and that isn’t the main cost of having the Vespa. Not needing any maintenance in 2021 will be the big savings consequence of working from home.

Extra food was 1005,55 euro. I am going to be honest, the only reason this is lower than last year is because of the pandemic and working from home. Working from home means the shop is further away. So just external circumstances, not an improvement in my discipline.

Gifts were 264 euro. Hey, the girlfirend doesn’t get a shiny gift every year.

Hobbies: 449 euro. Most is actualy trying to get a side gig off the ground but since it is not bringing in any money at all I have put these expenses under hobby.

Random fun: 1 019 euro. With nowhere to go I bought several games on steam. But also a laser and fog machine to be able to have the club experience at home (no lockdown parties here but I do hope social restrictions can be lifted somewhat so I can put this equipment to use again).

Restaurant: 145 euro. This is one restaurant visit with the parents because hello Covid.

Sports: 174 euro. This was 64 euro for swimming until the pandemic shut this down and then 110 euro for extra weights for my home gym

Telecom: 150 euro because I have a very cheap mobile viking subscription.

Health spending was 60,5 euro at the doctor/dentist and then another 164 euro at the pharmacy (mainly glasses for 147 euro). Not getting sick turns out to be cheap.

Hobbies: 449 euro Most of this expense is actualy trying to get a side gig off the ground but since it is not bringing in any money at all I have put these expenses under hobby.

Clothing: 92 euro

Travel: 1 220 euro. This amount covers our 10 day holiday to Portugal.

If I repeat the exercise of last year and look at the money i spend on stuff for me I liked buying I end up with 2 333 euro. A little bit up from last year but not by that much. Most of the up can actually be explained by games on steam and one could argue if these are that good for me. On of my goals last year was to spend more on funn stuff for myself but I honestely struggeld with this one. It seems I just don’t need more stuff.

2021 goals

Making goals for the new year is pretty futile since Covid is making a lot of things uncertain. Main things are still that I need to lose weight and get a somewhat interesting, fun side gig.

With no more expenses for the side gig and my end of year work bonus being paid, December should be a great month for savings. Let’s have a look.

Income: 3 729,15 euro

Expenses: 1 505,90 euro

Savings : 2 223,25 euro or 59,62%

Income:

Woohoo for the income!

Most of it, 3 679,15 euro was work income. My regular mothly wages + the end of month bonus. The remaining 150 euro was from christmas gifts from the parents and my mother-in-law.

Expenses:

I may, or may not have come in under budget this month depending on how you look at one particular expense this month. Mor e on that at the end of this post.

As I do every month I transferred 1 100 euro to our joint account to pay the mortgage, utilities and our joint grocery shopping.

Extra food was 100 euro. Being home helps me not buying extra food to eat during lunch. Especially because I now do my fitness during lunch break which just dossn’t leave me with any time to speed of to the nearest shop and buy some chips. I spend 60 euro on these extra snacks and then another 40 euro on pizza for me and a co-worker as the co-worker is leaving the compagny and pizza together was a bit our thing … Since he is leaving I paid for his pizza too.

Gas for the Vespa was 0 euro this month as I only drove it one time to work (and one trip to the shop to get some extra chips …). Which reminds me I need to take it for a spin in January and pump up the tires.

Mobile phone subscription for a bizare reason was only 2,5 euro. I have no idea why it was not it’s regular 12 euro and I am too lazy to find out.

Miscelanious expenses are a shampoo for 17 euro and a game on steam for 12 euro.

And then we come to the gift’s section where accounting my expenses has a tricky part.

The non tricky part is the 10 euro I chipped in for the goodbye gift for the co-worker keaving. And 130 euro I spend for end of year gifts for the family.

The tricky – acconting wise – part is the 100 euro I spend on buying Bitcoins. This because for a certain gift I needed bitcoins to pay for it. So I spend 100 euro buying bitcoins on Coinbase. But Coinbase also gives you a sign up bonus and allows you to ear some alt coins by watching some instructional videos (alt coins I off course exchanged into bitcoin the moment I received them). And then there was the incredibale value rise of Bitcoins in the second half of December… Long story short is that I bought the gift (which was 45 euro) but my balance on Coinbase is now close to 200 euro …

So did I just buy a 45 euro gift? Because, then I stayed below my 1 500 euro budget this year… or did I invest a 100 euro, bought the gift with part of my profits and still have another 100 euro in profit I should book? Since it’s a low amount. And since I am still not a fan of this whole crypto craze and will probaby use up the remaining balance in the future for other gifts, I just decided to book the 100 euro as an expense in the ‘random fun’ category.

Recent Comments